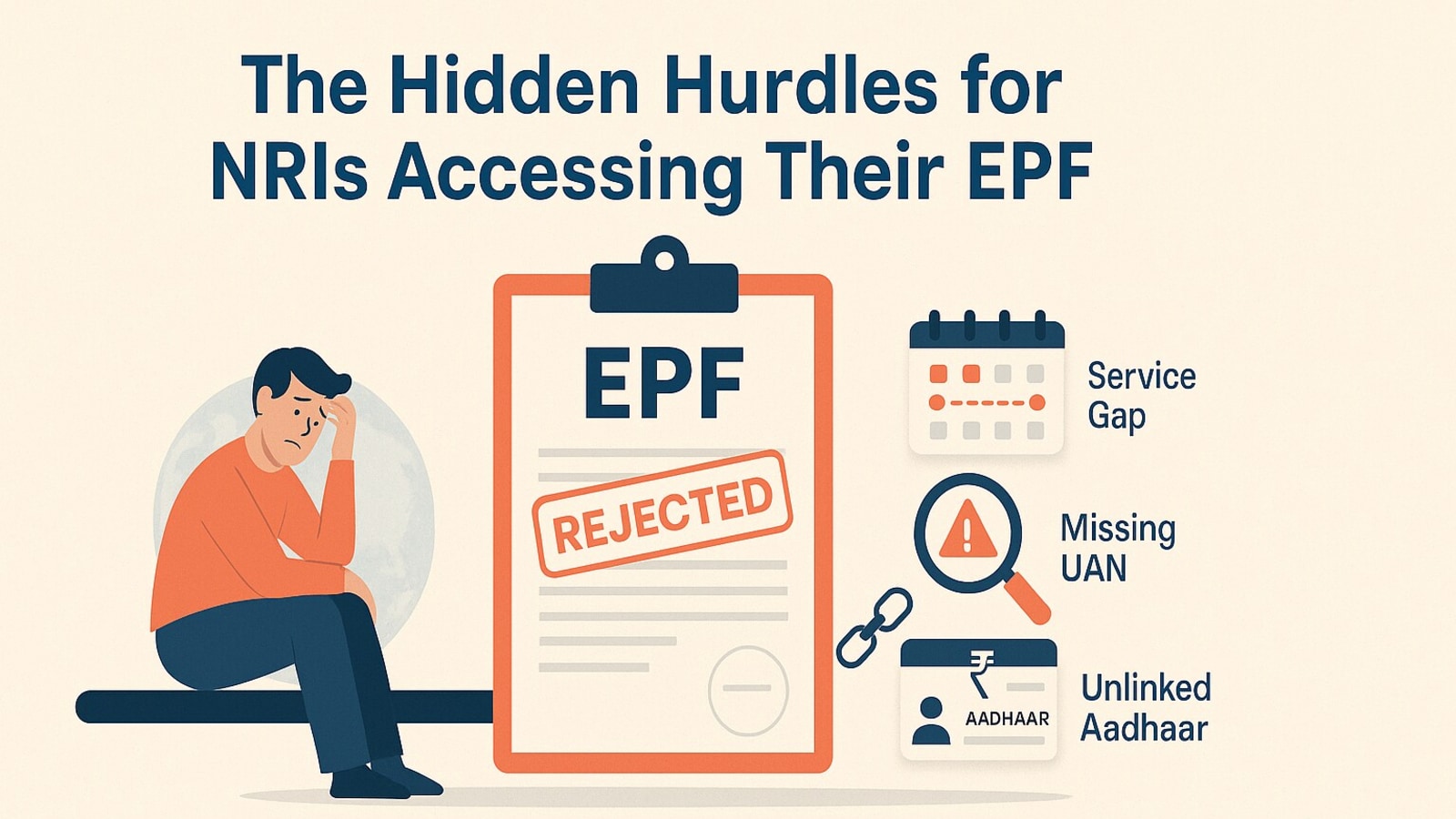

Across the world, Indians who once worked on home soil are finding their PF withdrawals tangled in red tape. Missed contributions. Unlinked Aadhaar numbers. Service overlaps. Whether they’re in Boston, Singapore, or Toronto, the stories are the same—the money’s there, but good luck accessing it.

Service gaps, missing UANs, dead-end claims

For some employers, the solution to sending employees abroad is simple: mark an exit date before they leave and a fresh joining date when they return. But that simple fix can come with a heavy cost. It creates a gap in service, disqualifying employees from gratuity, which requires five continuous years of service.

Read this | EPFO alert! How to avoid, deal with rejections, delays

Mr. A’s employer opted for a different route, keeping him on payroll but pausing EPF contributions while he was in the UK. When he returned, contributions resumed, but the EPFO now considers that year a break in service. The money’s in the account, but without the EPFO’s approval, it’s untouchable.

For those who left India before Aadhaar became mandatory, PF withdrawals can feel like navigating a maze without a map. Aadhaar is now linked to the Universal Account Number (UAN), the key to accessing EPF accounts online. But what if you don’t have one?

That’s the predicament facing Arvinder Gujral, who moved to Singapore in 2017. His last Indian employer, where he worked from 2014 to 2018, has since shut down. He has a UAN for that period, but the previous years (2009-2014) are unlinked. Without an Aadhaar link, he can’t access the PF member portal to resolve it. After filing multiple grievances with the EPFO and hitting a wall each time, he turned to a PF consultant. The case remains unresolved.

For NRIs like Gujral, the lack of a UAN or an Aadhaar link can effectively lock them out of their PF accounts indefinitely.

Boston-based Manish Maheshwari faced a different challenge.

While transitioning between two employers, Maheshwari exited one and joined the next on the same day, resulting in a service overlap. The EPFO rejected his EPF withdrawal request, and the situation became even more complicated after he moved abroad. “My physical presence at two different PF offices was required, which wasn’t possible. I got in touch with KustodianLife (a fintech with PF expertise) to get it done,” said Maheshwari.

One particularly tangled case involves a woman with a Canadian passport marked as an International Worker (IW) by some employers and as an Indian by others.

Despite her Canadian passport being linked to her EPF account, some contributions were made under Indian worker rules, which are different from IW rules. “Her PF history is a total mess,” said Kunal Kabra, founder and CEO of KustodianLife. “She may have to deposit an amount with the EPFO to settle previous records since IW contributions are higher than those of an Indian employee.”

Read this | Plan to withdraw from EPF for marriage, education, or illness? Know the rules

Kabra also noted a recent difficulty: earlier, the EPFO would share a detailed ledger of a member’s account upon request, which helped track service history, especially for NRIs who had been away for years. “Now that ledgers have stopped, tracking their service history is too challenging without online access,” he said.

How to navigate the PF maze as an NRI

The good news? There are ways to prevent these complications. Here’s what NRIs need to know.

If you are going abroad on the payroll of an Indian company, familiarize yourself with the Certificate of Coverage (CoC) and the list of countries with which India has a Social Security Agreement (SSA). “If posted to an SSA country, ask HR to obtain a CoC from the EPFO and submit it to the host country’s authority to avoid dual social security deductions. CoC is typically valid for five years,” said Ketan Das, PF Business Head, FinRight.

However, if going to the UK or the US, which do not have SSAs with India, contributions may be required both in India and the host country, according to Das. Note, as part of the recently announced India-UK deal, Indian employees on intra-company transfers may not be required to pay social security contributions in the UK.

Some employers may stop EPF contributions while you are abroad.

“If an employer is insisting on doing the full and final settlement while you are almost eligible for gratuity, you should negotiate to get the equivalent amount as ex-gratia in F&F (full and final settlement). Some employers keep the employment active without making PF contributions. They should be ready to explain it to the EPFO on behalf of employees about non-contributory service period,” said Anurag Jain, co-founder and partner at ByTheBook Consulting LLP.

Whether you are on an Indian company’s payrolls abroad or of a foreign company, your status will change to International Worker.

“Your contributions will be made as per IW rules in which 24% PF deduction happens on the gross salary, not basic salary. Moreover, you cannot withdraw from EPF while you are employed there,” said Das.

Read this | How NRIs can overcome banking challenges and manage their finances back home

Gross salary is your total salary without any deductions. Basic salary is usually 40-50% of your gross salary. So if your gross salary is ₹1 lakh per month, your basic salary could be ₹50,000. An IW will be contributing ₹24,000 (24% of ₹1 lakh) to EPF, while an Indian worker will contribute just ₹12,000.

Planning ahead

If you are moving abroad permanently, you must withdraw your PF. EPS withdrawal is possible only if the total service period is less than 10 years.

“If moving permanently and want to withdraw, initiate the process online via the UAN portal. For EPS, if they haven’t completed 10 years, they can withdraw the pension portion along with EPF (Form 10C). If they have crossed 10 years, they are eligible for a Scheme Certificate, which should be retained for future pension claims.” said Jain.

Update KYC and complete other important tasks. “Link your PAN, Aadhaar, bank account, and mobile number to EPF account through the UAN portal. Ensure the PF amount is consolidated into the last account and the date of exit is updated by the last employer. Link an active Indian bank account (Savings/NRO) to receive PF,” said Das.

The cost of inaction

If an NRI doesn’t withdraw their PF within three years of the last contribution, the account turns inactive and stops earning interest. The EPFO won’t automatically register NRI status unless it’s explicitly stated. Interest may continue to accrue beyond three years, but if the EPFO discovers the NRI status during the claim process, the withdrawal could be denied.

“There is a common misconception that PF withdrawals made after five years of continuous service are entirely tax-free. While the principal amount and interest earned during active service are tax-exempt, this exemption applies only if the withdrawal is made immediately upon cessation of employment. If there is a delay between the end of employment and the actual withdrawal, the interest accrued during that interim period is treated as taxable income,” said Jain.

Also read | Why missing your EPF nomination could leave your family in limbo

Additionally, check for a Double Taxation Avoidance Agreement (DTAA) between India and the country you are moving to, as it can help avoid dual taxation, he added.