In August 2024, India’s second largest business-to-consumer (B2C) logistics firm, Ecom Express, filed for an initial public offering. Valuation: nearly ₹7,500 crore.

This month, the company was sold to its biggest competitor, Delhivery, for less than half that amount.

In between, both the companies had an awkward spat via stock exchange filings. Ecom Express had claimed in its draft prospectus that it performed better than the much bigger Delhivery on some key metrics, including cost per parcel. Delhivery countered it by saying Ecom Express may be lying about its numbers.

None of it matters now. Earlier in the year, Ecom Express put its public offering plans on pause and began downsizing aggressively. And by April, it was sold. The biggest reason for its decline is well known: more than half of Ecom Express’ revenue came from a single client that most in the industry say is Meesho, the tier-II and -III focused e-commerce platform. In February 2024, Meesho launched its own in-house logistics arm called Valmo and reportedly stopped using Ecom Express’ services for most of its shipments. Bereft of its biggest client, Ecom Express quickly spiralled downwards and could not stick the landing on the best way out: a public listing. Acquisition was the next best outcome for its investors—the list includes PE firm Warburg Pincus and impact fund British International Investment.

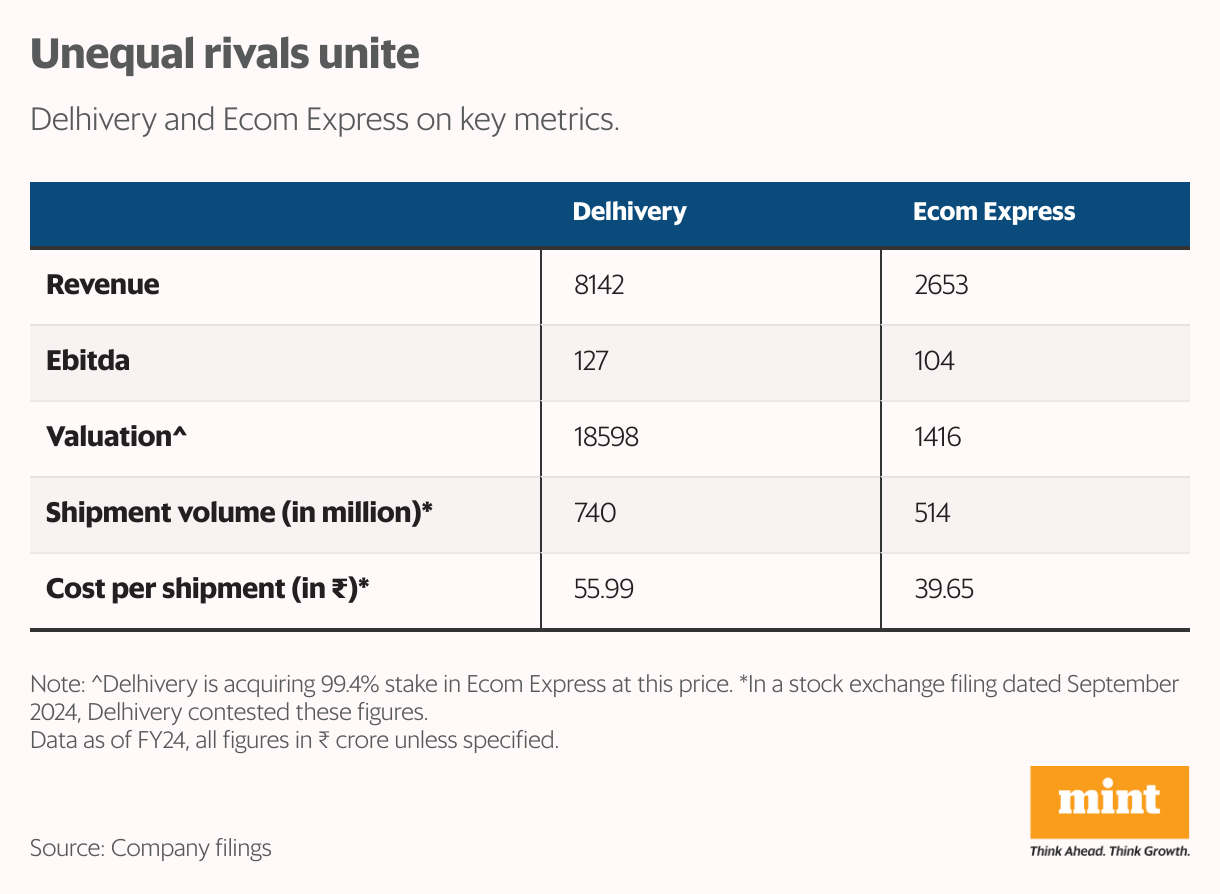

It is clear why Ecom Express needed a deal with Delhivery, even at a paltry valuation. With a deal size of ₹1,407 crore, Ecom Express is selling for roughly 0.6x enterprise value-to-sales (EV/sales), based on its financial reporting for FY24.

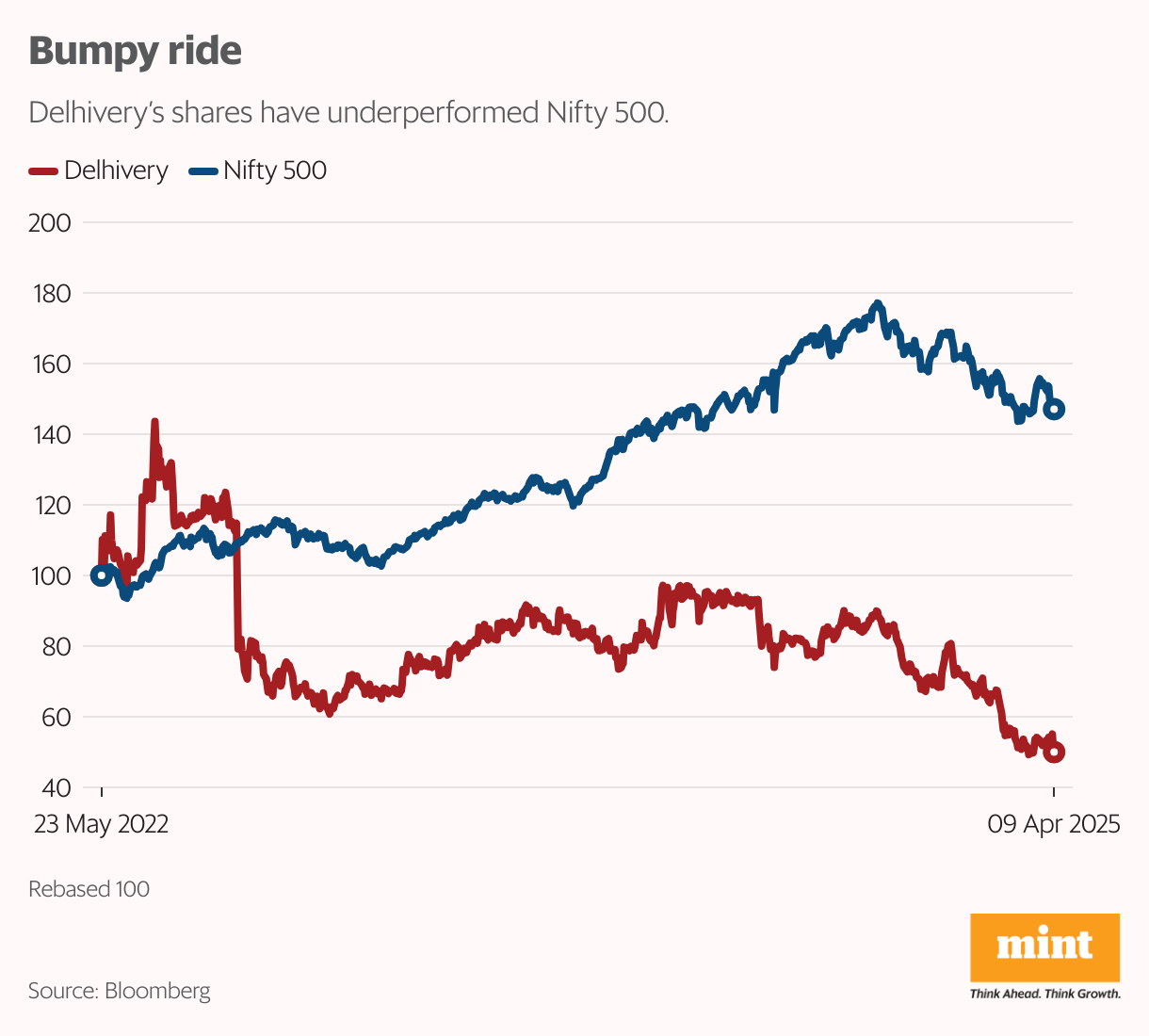

But what’s in it for Delhivery? The market leader has been struggling with profitability and poor market performance since it listed in May 2022. Can acquiring Ecom Express help it navigate the shifts in India’s e-commerce logistics business?

Shaky rationale

Analysts tracking this segment of logistics—B2C third party (3PL) surface logistics—are divided. A spokesperson for Delhivery declined to comment, saying the company is still waiting for approval from the Competition Commission of India for the deal. An Ecom Express spokesperson declined to comment, too.

Equities brokerage firm Emkay wrote in a note this week that acquiring Ecom Express could help Delhivery save significant costs.

“We expect significant cost synergies to accrue over the next 12-18 months, as Delhivery could rationalize the overlapping network infrastructure like sorting hubs, processing, delivery centers…” the report stated. “The combined entity would command ~55-60% market share of the 3PL B2C express market, dwarfing the immediate peer by ~3x.”

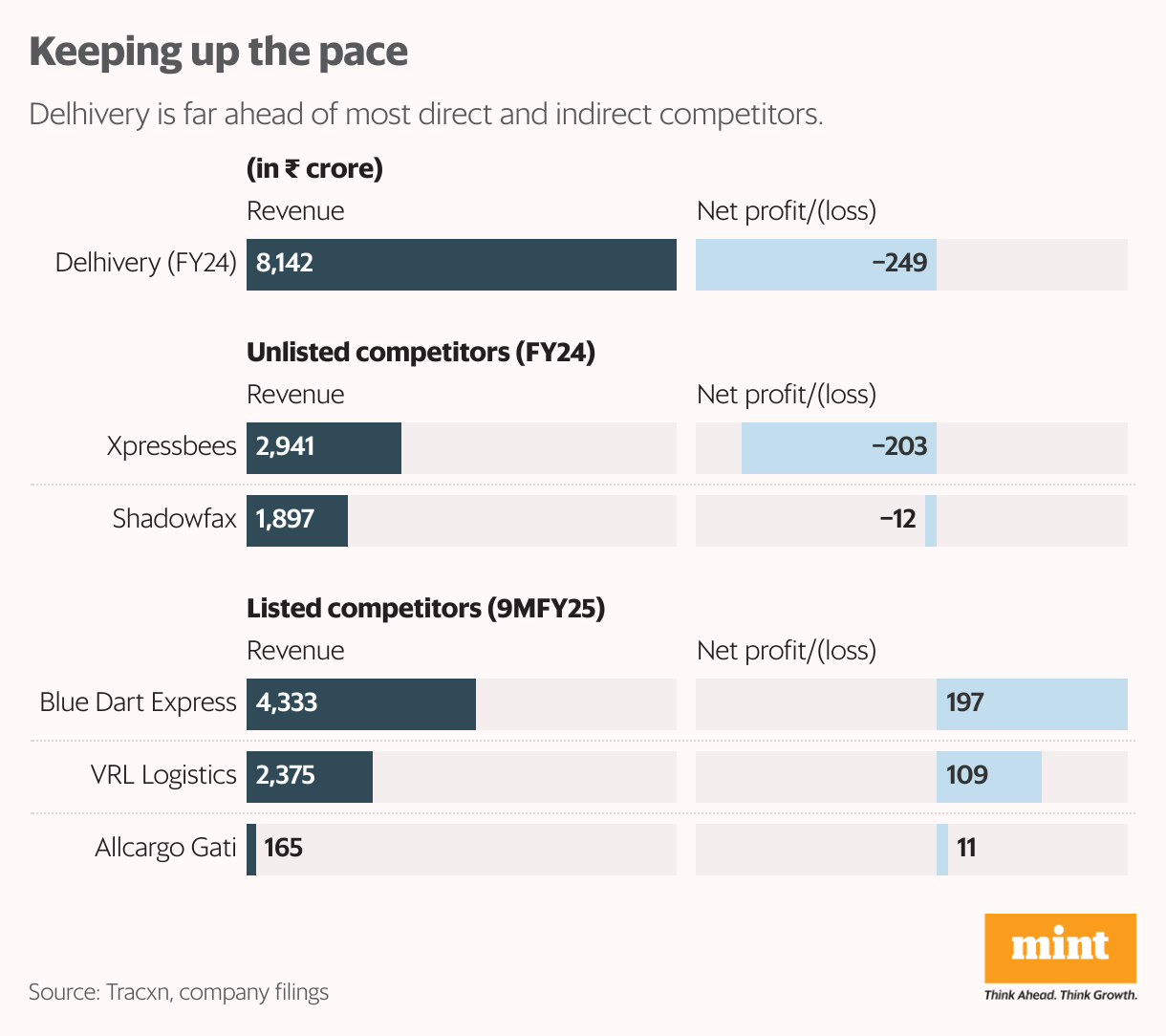

Other major firms in this segment of the logistics business include XpressBees, formerly the in-house logistics arm of baby products e-commerce marketplace FirstCry, and Shadowfax. Besides these, legacy courier companies also do some express B2C deliveries for online sellers, such as Blue Dart Express and Allcargo Gati.

“There are several advantages to Delhivery from this deal,” another senior equities analyst tracking the firm told Mint requesting anonymity. “First, the competition in this segment is reduced. That means the pricing disruption that was going on will also be reduced. After the merger of these two firms, the only major player left will be XpressBees. Both of them will figure out that there is no point depressing prices anymore,” the analyst explained.

With massive funding fuelling competition for the B2C logistics pie, firms in the business had begun undercutting each other over the last couple of years. This became more pronounced after Meesho started Valmo. “It’s hard to call out exactly how much prices fell across the board, but in general, these firms could not pass on any of their rising input costs to their customers,” the analyst quoted above said.

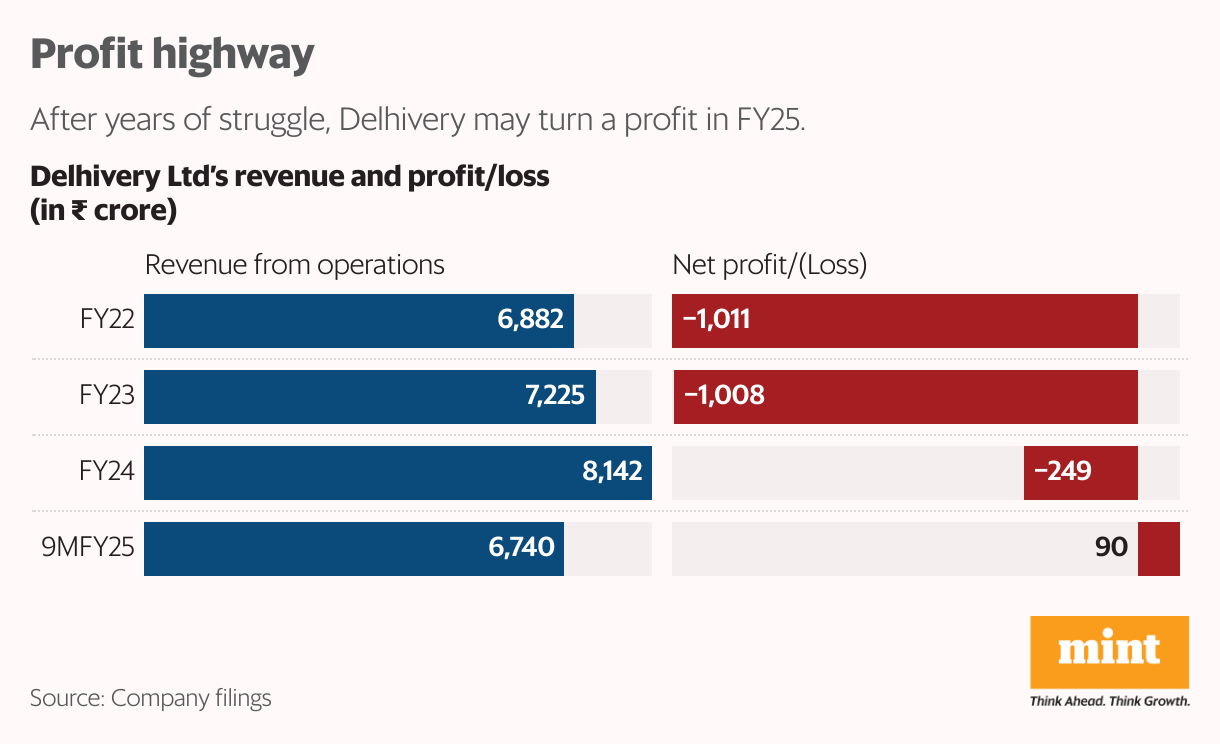

That was one of the reasons why both Delhivery and Ecom Express have been struggling with losses, although the former turned its fortunes around, starting FY25.

Some analysts tracking the sector say there is little long-term value in the deal.

“Yes, this is a nice deal and no doubt Delhivery’s market share will go up,” Rajarshi Maitra, associate director at equities research firm InCred Research Service told Mint. “But this market share will not move up by a lot. Ideally, the deal should reduce your cost per parcel and per unit of volume shipped. Right now, the cost per parcel in express delivery for both companies seem to be similar even though Delhivery’s volumes are 1.8x higher than that of Ecom Express. Even their Ebit margins (earnings before interest and taxes) excluding other income, are similar,” he added.

The implication here is that given the significant overlap in the business, it is difficult to see what more value Delhivery can squeeze out of the already flailing Ecom Express. When it deferred its public listing in February this year, the company had fired at least 500 employees and shut down major hubs, delivery centres and stopped serving about 3,000 pincodes in an attempt to cut costs, Mint had reported. There may not be much more room for cost cutting.

Although Delhivery is nearly three times bigger in size, consulting firm Redseer estimated that its cost per shipment was significantly higher than that of Ecom Express. In a report from August 2024, prepared for Ecom Express’ IPO, Redseer stated that the cost per shipment for Ecom Express’ express delivery was ₹39.65 in FY24 and nearly ₹56 for Delhivery. (Note: cost per shipment was calculated as the difference between the revenue and Ebitda of Delhivery’s express delivery business, divided by the total number of express shipments in the year). Ebitda is earnings before interest, taxes, depreciation, and amortization.

However, Delhivery contested this and other benchmarks that Ecom Express offered potential investors in its draft IPO documents. In September last year, Delhivery filed a note with the BSE that accused Ecom Express of misrepresenting these numbers. The key accusation it made was that the company was likely counting ‘return to origin’ or RTO orders twice, thus inflating its total number of shipments in a year and artificially bringing down its costs per shipment. It also alleged that Ecom Express was inflating the number of pincodes it serves, far exceeding the total number of pincodes in India altogether, as per government records.

Ecom Express did not address these allegations. But given this background, how much efficiency or economies of scale can Ecom Express bring to the table for Delhivery?

Bad history

Besides, InCred’s Maitra points out, Delhivery’s last major acquisition was a drag on the company’s performance. In August 2021, it bought Bengaluru-based SpotOn Logistics, a part-truckload (PTL) business that delivered goods to several businesses by clubbing together their relatively small orders into larger trucks. Delhivery was already running a PTL business which it planned to merge with SpotOn to expand the vertical.

The acquisition ran into trouble.

“The overall process of integrating the infrastructure and the network took longer than we originally expected,” Delhivery’s co-founder and chief executive officer, Sahil Barua, had told investors in an earnings call in August 2022.

View Full Image

In FY24, SpotOn made losses worth ₹24.9 crore on revenue from operations of ₹230 crore. Delhivery had invested ₹1,512 crore in the business in FY24, as per its annual report. In February, Delhivery’s board finally approved a resolution to merge both businesses with the parent firm.

As InCred’s Maitra also said, Delhivery’s acquisition of SpotOn has not paid off yet. Consider this: Delhivery’s revenue from the part-truckload business fell from ₹1,692 crore in FY22 to ₹1,546 crore in FY24 while tonnage in PTL freight tonnage was 1,429 thousand tonnes, lower than FY22, per the company’s annual report.

This, despite the big headroom for growth in the truckload delivery business. In the report quoted above, Redseer said that the full- and part-truckload logistics business is “highly fragmented” with three-fourths of the segment run by owners of small fleets of smaller, run-down trucks. “Compared to the B2C e-commerce logistics, which is largely organized as of FY24, FTL and PTL logistics invite limited organized competition with ~90-92% and ~60-70% unorganized markets respectively,” the report said.

Integrating Ecom Express will come with its own set of challenges, although unlike SpotOn, its business is nearly identical to Delhivery’s core express deliveries business.

“There will be some drag on Delhivery’s numbers for a couple of quarters although the extent of the impact remains to be seen,” the equities analyst quoted above told Mint. “My sense is that Ecom Express is losing about ₹10 crore a month. With that high a burn, there will be some impact on the books. Delhivery will have to cut costs quickly,” the analyst added.

There will be some drag on Delhivery’s numbers for a couple of quarters.

—An analyst

Corporate overheads will be among the first costs to go, the analyst said, because they were 5-6% of the company’s revenue last year. Besides, there will be overlapping warehouses, fleets, and fulfillment centres that Delhivery will have to streamline. In short: Delhivery’s financial turnaround may suffer in the short-term, perhaps a quarter or two.

Shifting sands

Despite these challenges, consolidation in this ‘new age’ logistics segment has been scant. In fact, just this February, Barua had made it clear to investors in an earnings call that there were slim opportunities to buy assets in the business.

“…Volumes are highly concentrated for most of our competitors and so it’s not clear what value we should ascribe to those volumes,” Barua said. “It’s better to let discipline enforce itself. So, we’ll wait and watch. If the right consolidation opportunity becomes available at the right price, then obviously, Delhivery is a natural consolidator in the market. But I don’t believe it’s necessary for us to try to force anything at this point in time.”

Two months later, he had clinched Ecom Express in a distress deal.

View Full Image

“It is interesting to see that consolidation among these players is happening now and not earlier,” Maitra said. “E-commerce logistics was considered a sunrise sector and funding was relatively easy to come by. None of the big players were keen to take each other on.”

According to data from financial research platform Tracxn, XpressBees and Ecom Express have raised more than $300 million each over several rounds of funding with participation from prominent global investors including PE firms Warburg Pincus, Blackstone, and TPG.

Now, the bigger threat to 3PL providers is existing e-commerce players. First, Amazon, Flipkart and later Meesho brought their logistics operations in-house, leaving the likes of Delhivery and Ecom Express in the lurch. Now, for the past two-three years, Ekart and Amazon Shipping Services are also successfully expanding into third party logistics, offering their shipping services to direct-to-consumer (D2C) brands and independent sellers.

“If Amazon has 30-35% market share and Ekart is the same, then Delhivery at best has about 23-25% share of this market (before acquiring Ecom Express),” InCred’s Maitra said. “But Amazon India and Flipkart have very strong parentage. Both Amazon and Walmart can continue to burn money,” he added.

The bigger threat to 3PL providers is existing e-commerce players. First, Amazon, Flipkart and later Meesho brought their logistics operations in-house, leaving the likes of Delhivery and Ecom Express in the lurch.

Besides, quick commerce has also started eating into e-commerce’s share of consumer goods sales. Amazon (Now) and Flipkart (Minutes) are both late entrants to this business dominated by Blinkit, Zepto, and Swiggy Instamart. But these platforms are expanding their inventory to high-value items including fashion and electronics.

Meanwhile, ‘vertical’ quick commerce platforms such as Swish (food delivery) and Slikk Club (fashion) are raising VC funding and some D2C brands are beginning to offer quicker deliveries in big cities. 3PL logistics firms have spotted an opportunity in serving this client base, hoping to beat Amazon and Ekart in the race.

Earlier this year, Delhivery started a pilot for quick commerce two-hour deliveries in Chennai, Hyderabad, and Bengaluru with two “core customers” and another 15 planning to go live. The company plans to set up not more than 50 dark stores in each of the top eight metro cities where quick-commerce is growing fastest.

But, Delhivery’s Barua warned investors in a February earnings call that this may not become a vast money-making segment anytime soon. In one year, Barua said, Delhivery could only scale logistics for quick commerce to ₹80-100 crore.

Ecom Express, along with smaller rivals including Shadowfax, already began setting up infrastructure for non-grocery quick commerce deliveries last year, The Economic Times reported in August. Ecom Express’ assets for this segment—such as dark stores in the city—could be of value for Delhivery but it is unclear how much of its warehousing and dark store network the company shut down to control costs earlier this year.

In the long run, all third party B2C logistics firms will have to think hard on new growth triggers. India’s e-commerce story is moderating as it becomes bigger; new last-mile opportunities, such as quick commerce, may not be as lucrative; in-house logistics arms can easily take away business from 3PL firms.

“In this industry, we are reaching, in some senses, a reckoning,” Barua had told investors in the February earnings call. “The reality is that incremental capital flow into this industry is now going to be severely constrained. And I think in the interest of sustaining themselves as going concerns, the competition is going to have to look at their business models.”

Delhivery will have to do the same as well. Ecom Express may be among its biggest acquisitions, but it alone may not deliver the company to a more lucrative future.